Unhinged Fund Alert!

17

Fund: Bear Stearns Asset-Backed Securities Fund

Affiliation: Bear Stearns

Size: $900 M

Status: suspended redemptions

Losses: ?

posted by The Obfuscation Oracle @ 4:11 PM

0 comments

![]()

![]()

This blog is a record of my market thoughts and trades in real time. I started trading with my savings in January of 2007. My strategy is based on macroeconomics. My idol is George Soros. My style is based on identifying where mainstream market beliefs differ from mine. You may email me at levinegregoryj@gmail.com. Thank you.

17

posted by The Obfuscation Oracle @ 4:11 PM

0 comments

![]()

![]()

Did the media report an 8% loss for Sowood Capital in July? Try 50%+.

posted by The Obfuscation Oracle @ 10:06 AM

0 comments

![]()

![]()

#16 is here!

posted by The Obfuscation Oracle @ 12:47 PM

0 comments

![]()

![]()

#'s 14 & 15 !

posted by The Obfuscation Oracle @ 1:25 PM

0 comments

![]()

![]()

Nationwide, housing-related employment accounts for about 10 percent of the economy. "The 10 percent is a problem, but it's not something that's going to undermine the economy," Zandi said.

These pearls of wisdom (quoted in Reuters) come on a day when the market shows that it clearly does not understand that the housing depression is not a trend to fight. Mark Zandi is the chief economist of Moody's Economy.com. Right now ITB is -5%. CFC -4%, GS -4%, DJIA -235, 10yr Treasuries, +2% (flight to quality), TOL -5%, etc.

This is not the time to look for value in the homebuilders. The thing to consider is the trend. It is still a toddler. It has room to grow much bigger and spread. On top of that, the market clearly has a well-documented history of underestimating the problems.

DHI reported an $824 M loss for the second quarter. It had charges of $1.28 B. That's $4.07 per share. Their book value per share is $20.82. They just lost 20% of book. In one quarter. Does anyone still believe that book value means anything?

posted by The Obfuscation Oracle @ 9:10 AM

0 comments

![]()

![]()

The thought occurred to me: What is the relationship of collateral to comsumeables with regards to inflation? What prompted me to formulate this question was wondering why Great Britain, with a strong currency, has a bigger inflation problem than the U.S., with a very weak currency.

posted by The Obfuscation Oracle @ 2:01 PM

0 comments

![]()

![]()

Time to short more homebuilders, to maintain my exposure. Between ITB and CFC, I'm up about 25% on each, so I need to short more to maintain my exposure. I'm thinking of shorting more of the index.

"Housing is contracting at an accelerating pace, taking out with a vengeance the brief stabilization at the turn of the year," said Ian Shepherdson, chief economist at High Frequency Economics, a private forecasting firm.This looks to me like a case of just shorting more all the way down. As was said in the UBS analyst report on homebuilders earlier this year, "book value doesn't mean anything." In the 1990 housing recession, homebuilders traded down to 30% of book. Beazer Homes might be approaching that, but it's hardly an average yet.

The supply of unsold homes did drop by 4.2 percent in June to 4.2 million, which analysts said was a hopeful sign that the price declines may soon come to an end.I guess the drop in supply is better than a gain, but the supply versus sales increased to 8.8 months' worth. Ouch!

According to an article from the L.A. Times on Winterwatch, foreclosures are up 799% yoy for the second quarter of '07. The accompanying chart provides more information: during the last housing downturn, foreclosures didn't peak until the END of the housing recession. Bottom line, don't even start to look for a rebound until 2010.

posted by The Obfuscation Oracle @ 9:15 AM

0 comments

![]()

![]()

Trading has cost me 5% so far this year. That's unacceptably high. So, I bought PCU @ 115.01 to fill in the long side of my portfolio.

posted by The Obfuscation Oracle @ 1:35 PM

0 comments

![]()

![]()

13

posted by The Obfuscation Oracle @ 4:06 PM

0 comments

![]()

![]()

We're still at 11 (as far as I know). However, we now have answers to the Bear Stearns' funds. The Leveraged fund is worthless, and the other fund nine cents on the dollar, according to Marketwatch.

posted by The Obfuscation Oracle @ 9:22 AM

0 comments

![]()

![]()

My investment strategy for the moment is based on credit. The parts of the market that are facing tightening credit are homebuilders and financials. As the consumer is also under a credit squeeze, retail is also included. The sectors of the market that I am bullish on are foreign commodity stocks. I expect that a consumer crunch will hit manufacturing next, probably in the next six months.

posted by The Obfuscation Oracle @ 3:10 PM

0 comments

![]()

![]()

bought 1 Tribune (TRB) Jan '08 $25 put for 0.90. (TRBME.X)

posted by The Obfuscation Oracle @ 9:37 AM

0 comments

![]()

![]()

This story confirms that weakness has spread to retail and will continue to spread. "Economists still believe that the economy... will come in at a rate of 3 percent or better in the just completed April-to-June quarter." Hmmm... Three straight bad months of consumer sales data makes me doubt that the data will be good. Much of the number will be a reduction in inventories from the first quarter. However, with consumer spending sinking, that will put further pressure on GDP growth throughout the rest of this year.

posted by The Obfuscation Oracle @ 8:45 AM

0 comments

![]()

![]()

Reading the winterwatch today, several thoughts occurred to me.

posted by The Obfuscation Oracle @ 2:40 PM

0 comments

![]()

![]()

Seriously considering BSC puts. They will "announce losses" on their hedge funds on the 16th. In other words, they will show the world how well everything's been swept under the rug. However, if it's really bad, they'll try to get it over with.

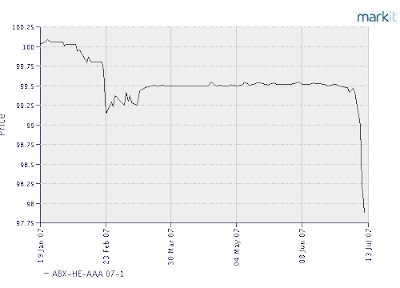

This is the best performing bond on the index. It's at 99.13 with a coupon of 0.11%. So, it's already lost 8 times the coupon. Ouch.

This is also AAA. It's lost 23 times the coupon. I don't know if the coupon is monthly or above Treasuries or what. I need to figure this out, but this definitely doesn't look like an investment grade product.

I believe these bonds work like the Titanic: the equity tranches fill up with losses first, then the non-investment grade bonds, then the investment grade. The higher rated bonds are no better than the worst; they just have a buffer. Once it's gone, they will sink just as fast as the worst junk.

The ratings agency's are broadcasting which bonds they might downgrade before they do, and delaying downgrades as long as possible. However, lawsuits like the one from Ohio's Attorney General will force downgrades. When the paper is downgraded, insurance co's and pension funds will have to sell the toxic paper. So, why are Moody's and S&P broadcasting the downgrades ahead of time? To allow anyone who can't hold junk bonds to sell, and get better prices than if they are forced to sell. They don't want this to come back and bite them if they can help it.

posted by The Obfuscation Oracle @ 3:40 PM

0 comments

![]()

![]()

# 11

posted by The Obfuscation Oracle @ 10:33 AM

0 comments

![]()

![]()

# 6 came in today.

posted by The Obfuscation Oracle @ 4:57 PM

2 comments

![]()

![]()

My strategy is big picture. I am fascinated by credit flows and how central bank and government policy interacts with global trends. I try to time bubbles, predict trend changes and invest accordingly. An inquisitive, contrarian, and skeptical attitude come to me naturally. I believe two things about investing. First, there are plenty of analysts who can pick out which snail (or tech company) will beat the other snails (or tech companies). What I want to know is, "Which asset class is the cheetah standing still?" This is what I have invested years of my time, energy, and thought process to do: understand the confluence of finance and economics and how to speculate on that knowledge.