Based on recent market developments, I am watching two trades. The first is a short position in EWC, the ETF tracking the MSCI Canada index. The second is long gold.

Why short Canada?

On the surface, Canada has a lot going for it. Their recovery seems firmly entrenched as commodity prices rebounded from the craters of early 2008. Last quarter, GDP grew at 6.1% annually. Joblessness has fallen in tandem with the recovery and is much lower than in the U.S. Canadian bank strength and capitalization is the envy of the world. Government finances are in much better shape than their southern neighbor.

On the contrary, all is not what it seems. Beneath the calm exterior, a storm is brewing. This storm is a product of two likely external factors. First of all, Canada is extremely dependent on the health of the American economy. The U.S. is Canada’s largest trade partner. Major exports are commodities, but manufacturing, including automobiles, is also export-dependent. This makes Canadian markets highly reliant on the American consumer. While not a consensus call, I believe that U.S. GDP will slow to negative growth by the fourth quarter. Along with this slowdown will come a sharp decrease in retail spending as high unemployment and deflationary credit conditions bite harder into the American wallet.

Second, China may be on the brink of a prolonged slowdown in GDP growth. For six months now, the Chinese government has been trying to delicately pop their real estate bubble. As a command economy, they might possibly be able to accomplish this without a market crash. However, construction and building is 50-60% of Chinese GDP, according to estimates I believe. This eats up a lot of commodities. Commodity producers represent a 43% weighting in EWC.

Finally, the Canadian housing market is rolling over. Major markets have shown the first sign of stress in recent months, as the Bank of Canada’s interest rate hikes take effect. Recently, the number of sales has fallen sharply, down 30% yoy in July. In major cities such as Vancouver, the decline in sales is even larger. Those who followed the U.S. housing crash were sensitive to the first tremors in late 2005/early 2006 as the number of sales dropped while prices continued to rise. This is a clear sign that credit driven prices may soon peak and the supply of greater fools is contracting. In the current environment of global austerity and credit contraction a housing downturn can easily become a full-fledged crash. I believe this is much more likely than market prices would indicate.

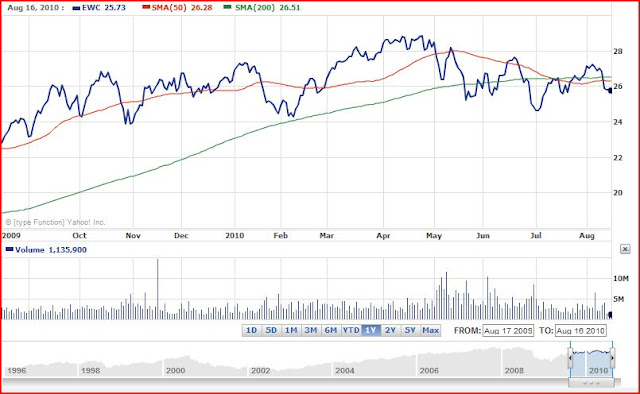

In conclusion, the market is not pricing in any one of these scenarios, let alone all three. Even if they are individually unlikely, the risk/reward on this trade is very favorable, in my opinion. Finally, the technical picture makes the timing ripe for this trade. The two year chart shows a possible head and shoulders pattern. Shorter term timing is indicated by a “death cross” of the 200-day moving average below the 50-day moving average on July 13. Even more recently, EWC was unable to maintain its breakout above the moving averages, and dropped back below on August 11. The chart I am referencing can be found here: http://finance.yahoo.com/echarts?s=EWC+Interactive#symbol=EWC;range=1y

I expect a sharp breakdown in EWC over the next six months. My practice is not to predict specific price levels, but to watch for changes in market behavior and sentiment. I will look to cover the short position on a combination of a jump in volatility, chart breakdown, and bearish market consensus. However, I will cut my losses if EWC breaks out of its recent trading range and climbs above $27.25.

Why gold?

Isn’t gold a hedge against inflation? And there’s no inflation to be seen, at least in the U.S. (No, there isn’t.) In fact, if the owner’s equivalent rent fiction is replaced in the C.P.I. model with the Case-Schiller home price index, inflation is -5% and falling.

But if gold was an inflation hedge, Treasury yields falling from 4% in April to 2.58% yesterday should not coincide with gold climbing from $1,125 to $1,225. So we can throw that idea out the window. Clearly there’s more to gold than an inflation hedge. Personally, I believe that gold climbs in periods of extreme interest rates, be they inflationary or deflationary. A deflationary environment, for example, makes gold attractive for two reasons. First, it is safe because it is not based on anyone’s promise to repay, and if held as bullion cannot be defaulted on. Second, low interest rates mean that cash can be held as gold without any great loss of interest income.

Over the first half of this year, almost all global economic policy actions have been deflationary. Fiscal policy has swung from stimulus to austerity and monetary policy has been tightened. In the U.S., the stimulus has been spent, states are enacting billions in spending cuts, and consumer credit is plunging faster than ever. The upcoming elections will most likely result in gridlock, and not conducive to economic stimulus. Tax cuts are just as likely as cuts in unemployment benefits and loans to bail out states. Europe has embarked on sharp austerity measures. China has imposed lending caps, raised real estate taxes, imposed higher capital requirements on banks, and forced them to move certain loans back on balance sheets. Japan is frozen solidly in deflation and sub-1% GDP growth. Canada has raised interest rates. Australia has raised interest rates. Got the picture?

The global supply/demand picture is also positive for gold. Many people in emerging market economies are hoarding gold. Last year, Vietnam instituted controls on gold imports as savers grew fearful that the global economic crisis would engulf their economy. China is also a large player in the global gold market. The People’s Bank of China has increased their gold reserves at an increasing rate in recent years. Gold is also the only commodity that the central bank of China can safely buy without increasing commodity costs for its export industry. China is also, by some reports, the world’s second largest producer of gold. I would not be surprised in the least if China embarked on a secret strategy to increase their gold mining industry while supporting the global price of gold. The Chinese government loves blowing bubbles to increase employment, and there aren’t many possible assets left. Mining is a labor-intensive industry, and China will need something to keep its construction workers employed.

That’s the fundamental macro-economic backdrop. Now for the technical analysis. I will use GLD for the ease of using Yahoo Finance! charts. The one year chart can be found here: http://finance.yahoo.com/echarts?s=gld. It shows GLD encountering resistance at the recent highs of $122-3 ($1,250-60). GLD survived a test of the 200-day moving average and made a recent low on July 27. Since then, it climbed above the 50 day moving average last week on August 12. In my opinion, it looks poised to break out significantly.

If I am wrong, I expect GLD to drop back below the 50-day moving average and will sell at $115. In the meantime, I will watch for any news relating to gold and China. If gold rises parabolically, I will consider taking profits and rebalancing my position if it climbs 20% over the 50-day moving average.

Disclaimer: The above analysis is not a recommendation to buy any security. It is merely my own personal opinion on positions I may or not participate in. Investments should take into consideration investor risk tolerance, time horizon, and sophistication.

Full Disclosure: short EWC, long gold bullion, long several gold stocks, long gold stock calls.